What If You Live Longer than Planned?

Feb 16, 2023

One of the major breakthroughs over the last century has been increasing life expectancy. In 1900 in the U.S., life expectancy for a woman was 48 years; in 2021, it was approximately 80 years. Pandemics aside, life expectancy continues to climb, especially for the college educated. Some experts, such Dr. Roizen of the Cleveland Clinic and author of The Great Age Reboot: Cracking the Longevity Code for a Younger Tomorrow, expect advances over the next decade that will add more years – in cases, a decade or more – to life expectancy among healthy people.

Life Expectancy vs. Longevity Risk

However, average life expectancy does not help much for individual planning. As a recent WSJ article highlights, what matters for most people is the life expectancy and longevity risk for their specific age group going forward. More desirable is to factor in specific conditions about one’s life that provide a more informed expectancy based on health and lifestyle habits. The Society of Actuaries and American Academy of Actuaries provides such a tool: Actuaries Longevity Illustrator.

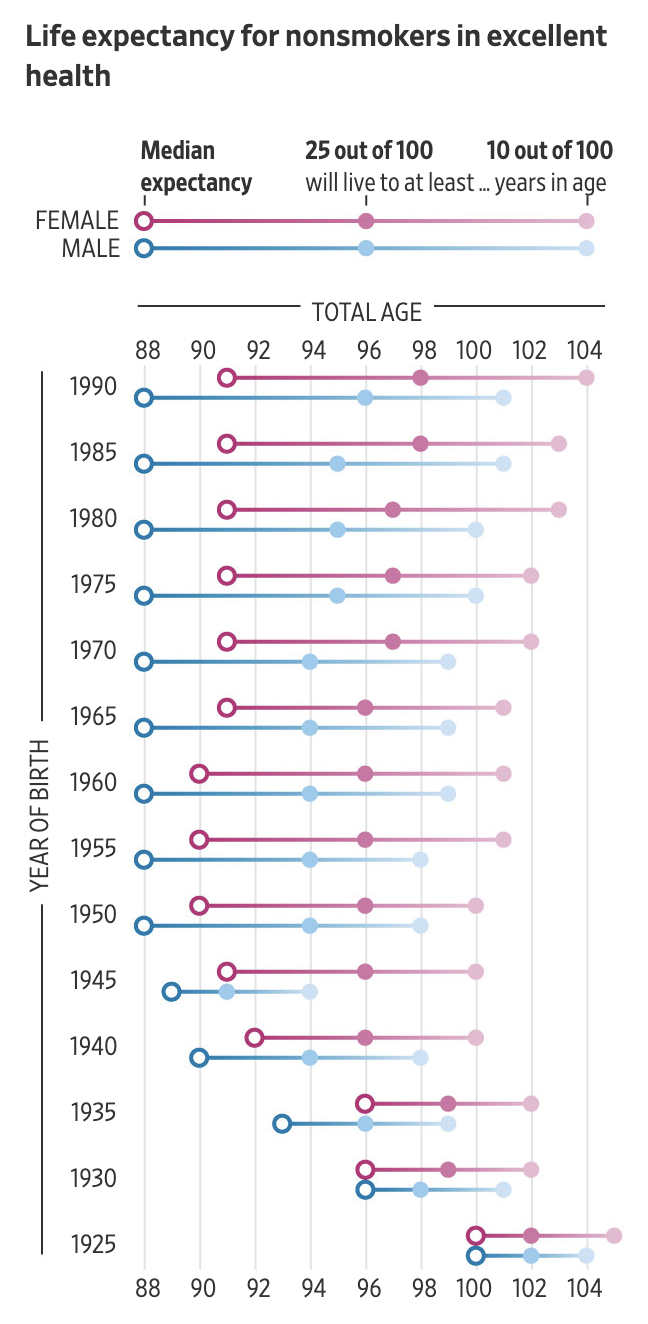

How long you live can be a moving target (Source: WSJ based on data from American Academy of Actuaries and Society of Actuaries)

For example, while the average life expectancy of a woman born in the U.S. in ’20 was approximately 80 years, the median life expectancy for a woman born in 1960 (age 63) who is a non-smoker in excellent health is 90.

For proper planning, we are best to think in terms of probabilities and understanding our personal risk tolerance. A healthy, non-smoking 63-year-old woman today has a 25% chance of living to 96 and a 10% chance of living to 101. Which probability outcome should planning scenarios focus on?

Also, keep in mind that these estimates are subject to change if Dr. Roizen’s longevity predications hold true. He estimates that today’s 65 year-old woman may live until 110, another roughly 20 years than currently expected, based on possible health advances.

Plus, according to research by University of Michigan’s Health & Retirement Study, people typically underestimate how long they will live. There are a few theories as to why but one thought is that people simply don’t want to think about it.

There are a number of implications related to the probability of living longer and our general inability to accurately forecast these probabilities.

Key Implication #1: Do The Work to Get a More Accurate Longevity Forecast

Work with a financial planner or actuarial – or lean on credible online tools – to assess your life expectancy and associated probabilities. Consider your risk tolerance. Some are comfortable generally planning for median life expectancy; others will only feel comfortable if 90%+ of scenarios are covered.

For couples, note that you must consider the probabilities that one spouse significantly outlives the other. Also, couples need to come to terms with an agreed risk tolerance.

Update your calculations on a regular basis or when significant life circumstances change.

Key Implication #2: Invest in Wealthspan & Healthspan

The longer one is likely to live, the more likely one will exceed one’s wealthspan and healthspan. Think about specific ways you can lengthen each.

Regarding wealthspan, for younger people, this may mean embracing a longer career, as long as 60 years (see WSJ’s “Here Comes the 60-Year Career”). For older people, it may mean delaying full retirement, picking up gig jobs, and taking a closer look at minimizing expenses. Keep in mind that inflation eats at wealthspan and we may be entering an era where inflation will be higher on an ongoing basis than in recent decades.

With healthspan, the benefits of being active – even just moving on a regular basis – are true across the age spectrum. Much the same is true with diet and sleep. Investing in friends is critical.

Living Longer May Motivate Remodeling Projects to Enjoy Your Current Home for Longer (Photo by Sidekix Media on Unsplash)

Living Longer May Motivate Remodeling Projects to Enjoy Your Current Home for Longer (Photo by Sidekix Media on Unsplash)

Key Implication #3: Factor in the Role of Place

Place – where you live and how you engage in where you live – is foundational for healthy longevity. Choosing wisely has the prospect of enhancing lifespan, wealthspan and healthspan. Particularly if you are living in a suboptimal situation, the rewards of changing or moving are greater if you have a longer time horizon to reap the benefits.

It certain cases it may mean modifying your current place or how you relate to your place. For example, you can make design changes in your home to make it ageless (see work by TPD Architects for example). At the same time, you can make efforts to reconnect with neighbors or engage in new hobbies and activities to elevate purpose and social connection.

Particularly in cases where a move is in the offing, it will be important to make sure that a move factors in the realities of your expected and probabilistic lifespan. The buy vs. rent calculus is critical and more nuanced than many may realize. Owning has the benefits of potential appreciation but the ongoing costs can be higher and more unpredictable than renting.

Longer Lifespans Require Greater Responsibility

17th century Philosopher Thomas Hobbes once described life as “solitary, poor, nasty, brutish and short.” Fortunately, this is becoming less common for people of contemporary times. Yet, longer lifespans require greater planning to optimize all that they offer. One of the first steps is to get an accurate gauge of specific the probabilities of a longer life. Alas, proper planning, including where to live for each life stage, depends on the quality of inputs.

Take the Right Place, Right Time Assessment

Are you in the right place for right now? This quick assessment will reveal opportunities to improve your life.

Subscribe to The Blog

We hate SPAM. We will never sell your information, for any reason.